![Day Trading Volatility Breakouts Systematically [All Rules Included]](/content/images/size/w1280/format/webp/2024/10/breakout-portfolio.jpg)

One of my primary approaches that I actively trade live within my systematic portfolios is intraday momentum trading. To implement this strategy effectively, I utilize Exchange-Traded Funds (ETFs) and futures contracts, as they offer greater efficiency on margin.

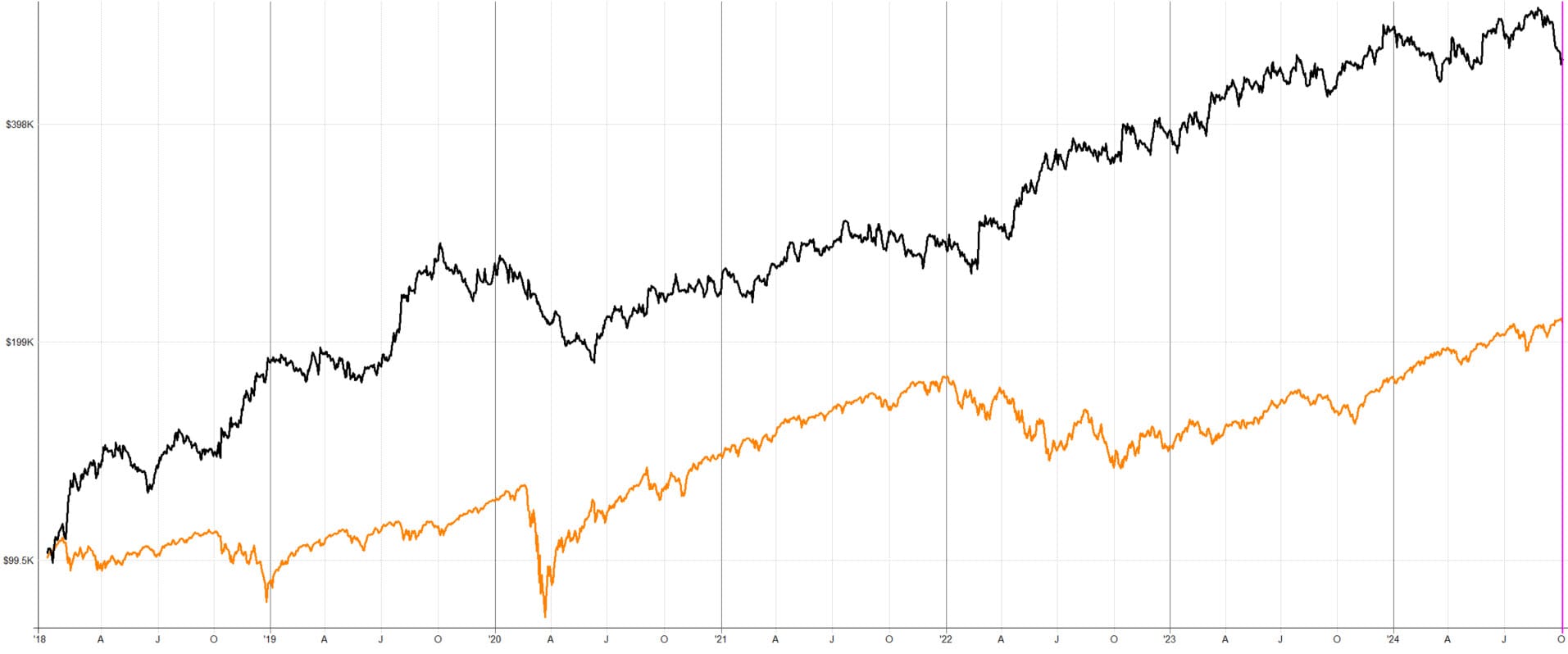

Below is the equity curve from a backtest conducted on the following markets:

- SPY (SPDR S&P 500 ETF Trust)

- IWM (iShares Russell 2000 ETF)

- QQQ (Invesco QQQ Trust)

- GLD (SPDR Gold Shares)

- USO (United States Oil Fund)

- DIA (SPDR Dow Jones Industrial Average ETF Trust)

Standard commissions from Interactive Brokers are included in the results. The backtests were performed using 1-minute interval data. I personally trade this strategy live and achieve similar performance characteristics.

Backtest Results

The backtest, spanning from 2018, encompasses a robust sample of 9,023 trades. Each trade is initiated with a strict stop-loss mechanism. By risking 0.33% of the account per trade, the strategy yields an annual return of 27%, with a maximum drawdown of -32%. The Sharpe ratio stands at 1.04, indicating a favorable risk-adjusted return.

Description of Trading System Rules and Live Trading Experience

The system employs a straightforward volatility breakout strategy. The specific rules for this model are as follows: